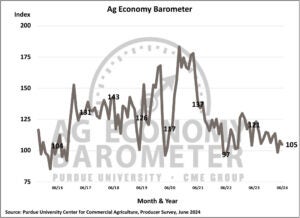

In June, farmer sentiment declined, as reflected in the Purdue University-CME Group Ag Economy Barometer, dropping to 105, which is three points lower than the previous month.

The sentiment dip was primarily due to a five-point decrease in the Index of Future Expectations to 112, while the Current Conditions Index slightly improved to 90, one point higher than in May. High input costs, the risk of lower product prices, and concerns about rising interest rates continued to weigh on farmers’ outlook. This data was gathered from the Ag Economy Barometer survey conducted between June 17-21, 2024.

The Farm Financial Performance Index saw a slight rise of three points, reaching 85 in June. In recent years, farmers’ financial performance expectations have tended to bottom out in the spring and improve as the growing season progresses. This trend appears to continue this year, with the index increasing by nine points over the past two months. Last year, similar improvements in financial expectations were driven by strong crop yields and a fall price rally. Whether these conditions will recur in 2024 remains to be seen.

The capital investment outlook weakened in June, with the Farm Capital Investment Index dropping three points to 32, just one point above its all-time low. More producers reported that now is a bad time to make large investments compared to May, with no change in the percentage who viewed it as a good time to invest. Concerns about rising interest rates appear to be influencing farmers’ investment decisions. The percentage of producers citing interest rates as a top concern has increased monthly, rising from 18 percent in February to 23 percent in June.

The Short-Term Farmland Value Expectations Index remained steady at 115 in June, while the Long-Term Farmland Values Index fell by seven points to 152. Fewer producers expect farmland values to rise over the next five years, with more predicting that values will remain unchanged. Among those anticipating long-term increases in farmland values, 57 percent attributed it to non-farm investor demand, and 16 percent pointed to inflation. Notably, 10 percent of optimistic respondents identified energy production as a key driver, a factor included in the survey for the third month.

Additionally, eight percent of respondents reported being approached about a Carbon Capture and Storage (CCS) project from an ethanol plant, with the majority (93 percent) offered payment rates of less than $25 per acre, and only 8 percent offered $50 or more per acre.

Sixteen percent of respondents discussed farmland leases for solar energy production within the last six months, a slight decrease from the 19 and 20 percent reported in April and May, respectively. Lease rates have been rising since 2021, with 69 percent of respondents in June 2024 offered long-term lease rates of $1,000 per acre or more, compared to 27 percent in June 2021. This month, 27 percent reported offers of $1,500 per acre or more, with 58 percent mentioning lease contracts that included an annual escalator clause, most commonly ranging from 2 to 3 percent per year.

Overall, the decline in farmer sentiment was driven by weaker expectations for the future. Concerns about rising interest rates likely contributed to the dip in future expectations, capital investment outlook, and long-term farmland value projections. In regions where solar energy leasing is prevalent, lease rates continue to rise, with 69 percent of those involved in solar leasing discussions receiving offers of $1,000 per acre or more.