National agricultural lender, AgAmerica, has released its 2023 U.S. Farmland Report, which digs into market recap of the year, financial projections for 2024, trends related to farmland ownership, and the current barriers/benefits of investing in farmland. Among one of the company’s biggest predictions: Roughly $1.5 trillion in farmland could exchange ownership over the next two decades.

AgAmerica believes that a wave of land ownership transfer is coming. When combined with the holdings of nonoperator landlords, half the farmland in the U.S. is owned by individuals who are at least 65 years old. If U.S. farmland is a $3.42 trillion market as research suggests, then that means nearly $1.5 trillion in farmland could exchange ownership in the next two decades.

Other insights include:

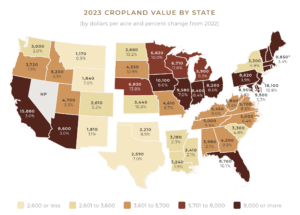

- The farm economy is approaching a decline, even as land values remain strong. A 22 percent decline in net farm income is expected in 2023, with a 4.3 percent drop in total farm cash receipts. At the same time, the USDA predicts a six percent increase in U.S. farmland values.

- Equity is a top risk management strategy landowners can leverage. For a farmer that owns their land, that land makes up over 80 percent of their assets. With more competitive rates and flexible terms than crop and equipment loans, land loans can be used as collateral to provide capital to increase operational profitability.

Over the past decade, U.S. farm real estate values have increased nearly 40 percent, which has allowed a hedge against inflationary pressures for rural landowners. On the other hand, this trend has also created higher barriers of entry (via capital, consolidation, and connections) for those aspiring to upgrade from tenant to landowner. While landowners have been able to leverage land equity to mitigate risk, tenant farmers are having to navigate higher cash rents and input costs without equity access in their corner.

As farm real estate values continue an upward trend, it’s important to understand the drivers involved to know where they could be headed in the coming years. They key drivers of land values this year have been cash rents, interest rates, commodity prices, parcel levels, and government policy.

While the U.S. farmland market has exhibited an overarching theme of resilience and profitability, there are significant variations across ownership demographics, farm size, and regional differences. For example, small farms represent nearly 90 percent of U.S. farms, but comprise roughly half of total U.S. farmland and less than 18 percent of total production. Since 2000, the share of farmland owned by operations that made $1,000,000 or more has increased from 9.2 percent to 25.7 percent.

This growth has slowed since 2012 but continues to be the trend. A steep incline in the share of large-scale operations between 2008 and 2012 coincides with the world economic crisis of 2008 to 2009 and the subsequent recovery. During this period, global recessionary pressures decreased demand for global trade of agricultural commodities, instigating low commodity prices and stifling the economic growth of smaller operations.

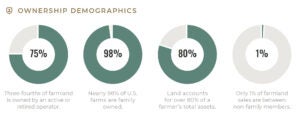

According to AgAmerica’s analysis, over 75 percent of American farmland is owned by an active operator or a retired farmer. Just over 60 percent of farmland is farmed by an owner-operator. Active owner-operators, retired farmers, or their families are the landlords on over half of rented farmland. In contrast, under three percent of farms are non-family owned — which includes land that is institutionally owned — and account for less than 14 percent of the total value of production.

The most successful farmers typically already own their own land. They not only create more long-term value on land they own, but also generate higher average farm income than lower quality operators. Additionally, larger operations tend to be more efficient in production than smaller operations due to economies of size, an advantage generated by increasing production and lowering average costs by purchasing in greater volume and spreading fixed costs across the increased production. This allowed larger operations to weather lower commodity prices better and put them in a stronger financial position to expand.

In terms of price discovery, just 1 percent of farmland trades hands in a sale between non-family members. The majority of that is sold farmer-to-farmer through an off-market transaction that avoids the use of a broker or auction. Farmers and their families set the price of farmland and determine the potential for active or passive farm income to be earned from farmland ownership.